Acquisitions continue to transform the HVACR industry. PE (private equity) are expanding their portfolio companies and others are seeking to enter the market. National distributors are expanding into new territories and also acquiring smaller companies as “fill-ins” or, in some cases, are diversifying their businesses and building new divisions. Regionals, and even some “local” independents are expanding their wings to achieve their next level of growth and pursuing acquisitions.

For some it is their growth strategy, for others it is a component of the strategy.

And for the seller, it is their exit planning, frequently because they do not have a succession plan.

When ownership seeks its exit, the options become to sell to a strategic firm, possibly to sell to a PE firm (especially if ownership wants to stay a little longer or is seeking an outside investor to support growth or replace an ownership interest), to consider selling to employees (and establish an ESOP), or potentially sell to the management group.

Acquisitions, mergers, ESOPs are all viable options to an exit strategy or in pursuit of a growth strategy.

Recognizing this is the industry’s future, I thought it may make sense to reach out to some experts to share insights into the structure of these deals.

Given the interest in acquisitions to power growth, and exit, strategies in the distribution and manufacturing community, I asked Geoff Ling, the Managing Director and Founder of Merrimack Group, to share some insights.

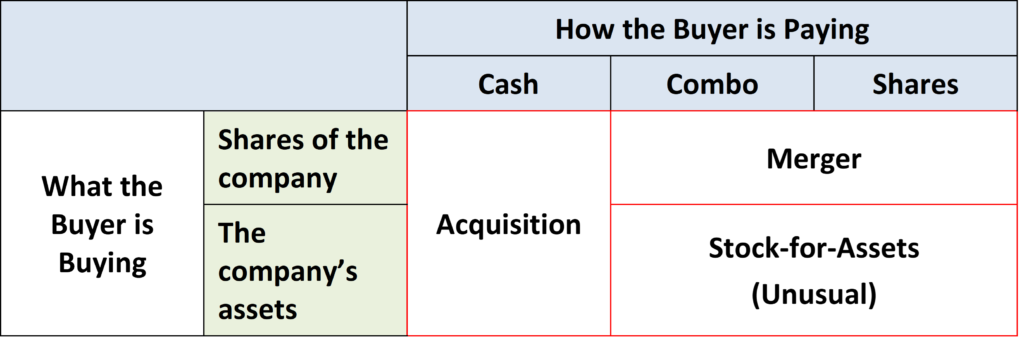

When Selling a Company Which is Better: A Stock or Asset Deal?

“Business owners invariably ask the above question when selling their business. It sounds like a technicality,  but it can have significant tax and legal implications. The short answer is a stock deal is better for sellers in most cases, but both scenarios should be carefully evaluated.

but it can have significant tax and legal implications. The short answer is a stock deal is better for sellers in most cases, but both scenarios should be carefully evaluated.

In a stock sale, the buyer purchases shares of the target company from the shareholders. The target company itself does not sign the sale and purchase agreement, although the management team typically facilitates the transaction. In most cases, a stock sale is better for the selling shareholders for two reasons:

- In the US (at least), the seller’s tax bill is lower because capital gains rates apply, and, if the company is taxed as a C-Corp, the seller avoids the double taxation. Double taxation occurs when the company pays tax on the sale of assets, then the shareholders pay taxes on the distribution. S-corps are pass-through entities (PTEs) in tax-speak, meaning that the company itself pays no federal tax (as a disregarded entity) but the shareholders are taxed at ordinary tax rates on their share of the company’s profits. So S-Corps are generally still better off with stock deals because capital gains rates are lower, even though they don’t have the double taxation problem.

- By default, the buyer assumes all liabilities that may pop out of the woodwork from pre-closing events, although buyers generally push for a provision providing recourse in the definitive agreement.

On the other side of the table, buyers generally prefer an asset deal because they can reduce their tax bill through deductions for depreciation and amortization, and because they are less likely to be held liable for pre-closing events. However, there are cases where buyers might prefer a stock deal:

- If the target company has accumulated net operating losses that can be applied to reduce the buyer’s tax bill.

- If the target company has contracts or licenses that cannot be easily assigned to the buyer, especially if the deal requires supplier / customer consent.

In practice, larger transactions (starting around $50 million) are generally structured as stock deals, assuming that there is a competitive bidding environment.

For smaller deals, the transaction structure is usually negotiated. We recommend that clients engage their CPAs at an early stage in the process to compare the tax consequences of a stock deal vs. asset deal. In many cases, state taxes can make a significant difference. We have seen a couple of deals recently where the sellers were essentially indifferent from a tax perspective.

If the seller has a strong preference for a stock deal, we are careful to communicate that to buyers so they can tailor their offers accordingly. Buyers with a strong preference for asset deals will understand that their headline number will need to be particularly attractive, since offers are ultimately compared on an after-tax basis. Sophisticated buyers sometimes run the numbers on both sides and propose the transaction structure that is least advantageous to tax collectors, i.e. maximizing the pie then dividing it.

Some clients ask if they should consider a merger. While we all read about mega deals in the headlines structured as mergers, they are not common in the middle market. A merger is essentially a stock deal in which the buyer offers its own shares, or a combination of cash and shares, to pay for the transaction. Mergers are generally offered only by public companies because private companies know that the sellers are unlikely to accept shares that they cannot easily sell.

A strong team of advisors is necessary to achieve full value and avoid costly mistakes. Merrimack recommends engaging an M&A advisor to conduct a competitive process, legal counsel with extensive M&A experience, and a CPA to analyze tax consequences.”

About Geoff Ling

Geoff is the founder of Merrimack Group, which specializes in helping distributor, manufacturers and reps in the construction trades companies with mergers and acquisitions. He earned an MBA from the University of Chicago and advised on 30 successful transactions amounting to $900 million.

Structure Acquistions Takeaways

- For owners facing a change in control, understanding your options is critical to the future of your staff, the perpetuity of your business, potentially your “legacy”, as well as the fiduciary responsibility to your key stakeholders (typically your family). Further, the decisions that you make can affect the growth plans of your company. There is much to balance and the time to do this is before you need to.

- Looking to make acquisitions? Understanding the different models helps you craft growth model strategies as well as determine financial commitments and your willingness for change in control or ownership interest.

- From interacting with owners, speaking with those who have sold and those who are acquirers, as well as companies that have (and are) considered ESOPs, the decision and negotiating time frame can be extensive … at a minimum six months, many times years of considering and courting (remember those days?!) It’s a process and potentially the biggest business decision (and sometimes a final one) that is made.

- There is lots to consider as you consider the right option. A 3rd party can add value as a neutral party to help you make the best decision.

- For non-owners, understanding what goes into the decision-making process can be helpful in understanding why some decisions are made.

Leave a Reply