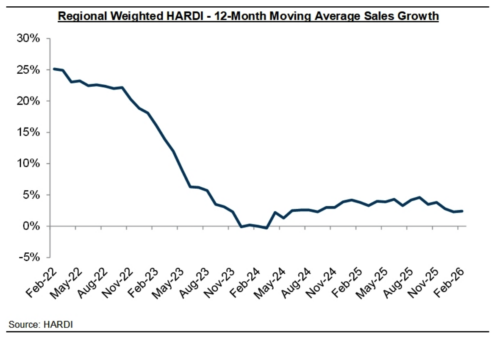

HVAC distributor sales moved in the right direction in February, with HARDI reporting weighted average same-day sales up approximately 5% year-over-year. That is a meaningful swing from January, when the same measure was down 1%. Before anyone calls it a recovery, though, it is worth looking at what is actually driving the number.

soft new residential housing are pressuring volumes. Light commercial is starting to see modest improvement.

Price Is Doing Most of the Work

Industry analysts tracking the sector estimate that pricing contributed roughly 8 percentage points to the February result. That means underlying unit volumes were actually down low single digits year-over-year. The dollar sales number looks encouraging, but the unit picture is more cautious.

This matters for how you read order flow, stocking decisions, and margin. When revenue grows because equipment costs more rather than because more units are moving, the operating picture is different than it appears on the surface. Distributors and reps should be careful not to let the headline number set the wrong expectations for spring.

Inventory Is Still Part of the Equation

HARDI inventories came in up 2% year-over-year in February. That gap has been narrowing, which is progress. But inventory remains elevated relative to where most distributors want it. If demand does not accelerate through the spring cooling season, working through that stock gets harder.

For distributors managing open-to-buy, and for reps whose lines are competing for shelf space and attention, inventory positioning is still an active factor in most branch conversations. The trend is moving in the right direction, but it is not resolved yet.

The Southeast Is Leading the Country

Regional performance varied in February. The Southeast posted same-day sales up 6%, outpacing the national average. That tracks with the region’s population growth and construction activity patterns. Reps and distributors operating in the Southeast have more reason for measured optimism than those in softer markets.

The regional split is a useful reminder that national averages describe the country, not your territory. Understanding where your specific market sits relative to the headline number is worth knowing before you take a position on what spring will look like.

What March and April Will Tell Us

February is seasonally light, which means one good month does not confirm a trend. The real test comes in March and April, the first meaningful read on cooling season demand. Analysts expect March same-day sales to come in up 2% to 3%. If that holds, and April follows, the case for a genuine market turn builds. If those months soften, February looks more like seasonal variation than a signal.

Two factors are worth tracking as the season opens. First, sticker shock on A2L equipment continues to push some residential replacement decisions out. Homeowners seeing the new price points are deferring, and that is suppressing some of the replacement volume that would normally flow through this time of year. Second, new residential construction remains soft, limiting new-install activity. Light commercial is beginning to show modest improvement, which is a better sign, but it is not yet confirmed as a sustained move.

For 2026, most manufacturers are planning for roughly flat unit volumes with mid-single-digit price increases carrying the revenue line. That context is useful for setting realistic expectations internally and with your channel partners.

What This Means for Distributors, Reps, and Contractors

For distributors, one positive month does not change the math on inventory or buying strategy. Spring stocking decisions should track actual order patterns, not the February headline. A disciplined approach tied to real demand signals is more defensible than loading up ahead of a trend that has not confirmed itself.

For reps, the regional variation matters. The Southeast-led number may not describe your territory. That context belongs in your conversations with manufacturers about program investment, stocking commitments, and sales expectations for the year.

For contractors, the pricing environment is not changing in the near term. A2L equipment costs are up, and the quoting process is more complex than it was two years ago. Getting in front of replacement decisions before the season peaks gives you more room to manage customer expectations and close jobs without the pressure of a full schedule working against you.

If this aligns with what you are seeing in your market, I would like to compare notes. CMG works with manufacturers, distributors, and rep firms who want clearer strategy, stronger channel performance, and better alignment across the field. If you are exploring ways to strengthen your commercial approach, reach out and let’s talk through what you are trying to build.

Leave a Reply